Navigating today’s complex risk environment can be a monumental task. Steve Shappell, Alliant Claims & Legal, spearheads Executive Liability Insights, a monthly review of news, legal developments and information on executive liability, cyber risk, employment practices liability, class action trends and more.

FEATURED ARTICLE

DELAWARE COURT OF CHANCERY RULES THAT OFFICERS HAVE DUTY OF OVERSIGHT WITH RESPECT TO SEXUAL MISCONDUCT CASE, CALIFORNIA COURT ADDRESSES SIMILAR ISSUE

In re McDonald’s Corporation Stockholder Derivative Litigation, No. 2021-0324-JTL (Del. Jud. Jan. 25, 2023)

Luke Kahnert, et al. v. Robert A. Kotick, et al., No. CV 21-8968PA (U.S. C.D. Cal. Jan. 17, 2023)

In Delaware, the Court of Chancery held, for the first time, that corporate officers may have the same duties of care and oversight as corporate directors. The matter arises from a derivative lawsuit brought by shareholders against the company’s board, the former CEO and the former Global Chief People Officer alleging breaches of fiduciary duty for failing to prevent a culture of sexual harassment and misconduct.

In This Issue:

DELAWARE COURT OF CHANCERY RULES THAT OFFICERS HAVE DUTY OF OVERSIGHT WITH RESPECT TO SEXUAL MISCONDUCT CASE, CALIFORNIA ADDRESSES SIMILAR ISSUE

In re McDonald’s Corporation Stockholder Derivative Litigation, No. 2021-0324-JTL (Del. Jud. Jan. 25, 2023)

Luke Kahnert, et al. v. Robert A. Kotick, et al., No. CV 21-8968PA (U.S. C.D. Cal. Jan. 17, 2023)

In Delaware, the Court of Chancery held, for the first time, that corporate officers may have the same duties of care and oversight as corporate directors. The matter arises from a derivative lawsuit brought by shareholders against the company’s board, the former CEO and former Global Chief People Officer alleging breaches of fiduciary duty for failing to prevent a culture of sexual harassment and misconduct.

Read More >>

BUMP-UP EXCLUSION PRECLUDES COVERAGE FOR MERGER LITIGATION SETTLEMENT

Komatsu Mining Corp. v. Columbia Casualty Co., 2023 U.S. App. Lexis 1639, No. 2:18-CV-02034 (7th Cir. 2023)

A federal appeals court held that an “inadequate consideration” or “Bump-Up” exclusion in a primary Directors & Officers Liability (“D&O”) policy precluded coverage for a settlement arising from a merger.

Read More >>

2022 TRENDS IN SECURITIES CLASS ACTION LITIGATION

Trends in securities class action litigation in 2022 showed drastic differences from years prior. For the fourth consecutive year, federal filings have declined because of fewer merger-objection and Rule 10b-5 cases being filed—from 431 cases filed in 2018 to only 205 filed in 2022.

Read More >>

DELAWARE INCREASES SCRUTINY OF SPAC DISCLOSURES

Delman v. GigAcquisitions3, LLC, No. 2021-0679-LWW, 2023 Del. Ch. LEXIS 1 (Del. Ch. Jan. 4, 2023).

Delaware toughened its stance on Special Purpose Acquisition Companies (“SPACs”) and subjected them to more scrutiny. Shareholders of a SPAC which acquired an electric vehicle start-up, claimed that it fared poorly for investors despite optimistic financial projections issued before the merger.

Read More >>

A JOINT VENTURE MEMBER SHOULD BE ABLE TO PRESENT ANY INFORMATION TO THE APPRAISER

A Delaware court ruled in favor of the majority owner of a joint venture company, in a dispute that alleged that the majority owner inappropriately intervened with the appraisal process of the minority company.

Read More >>

CONSTRUCTIVE NOTICE NOT SUFFICIENT IN THE CLAIMS MADE AND REPORTED WORLD

Evanston Ins. Co. v. Rodriguez Eng'g Labs., No. 1:21-CV-01129-RP, 2023 U.S. Dist. LEXIS 9885 (W.D. Tex. Jan. 20, 2023)

A Texas federal court ruled that an engineering firm (the “Company”) lost its coverage when it failed to timely notify its excess professional liability (“PL”) carrier of a claim timely. In the underlying suit, the company was accused of defective work on a project.

Read More >>

FAILURE TO COMPLY WITH NOTICE REQUIREMENT COSTS BANK EXCESS COVERAGE

Heritage Bank of Commerce v. Zurich Am. Ins. Co., No. 21-cv-10086-RS, 2023 U.S. Dist. LEXIS 383 (N.D. Cal. Jan. 3, 2023)

A California district court ruled against a bank in its effort to compel coverage from two layers of excess insurance. The insured bank failed to provide proper notice to the excess carriers in the tower of insurance during the policy period.

Read More >>

CONTRADICTORY COMPLAINTS LEADS TO DISMISSAL ON ALL ALLEGATIONS

Underwood v. Coinbase Glob., Inc., 2023 U.S. Dist. LEXIS 17201 (S.D.N.Y. Feb. 1, 2023)

A New York federal court ruled in favor of a crypto exchange (“Exchange”) after cryptocurrency buyers (“Buyers”) failed to prove that the exchange was an “immediate seller” of securities. This action was brought on behalf of a nationwide class consisting of all persons or entities who transacted in securities on the Exchange’s trading platform.

Read More >>

IN A COMPETING CLAIMS SCENARIO, INTERPLEADER IS APPROPRIATE

QBE Specialty Ins. Co. v. Kane, No. 22-00450 SOM-KJM, 2023 U.S. Dist. LEXIS 14705 (D. Haw. Jan. 27, 2023)

A Hawaiian court agreed to deposit the remainder of a directors and officers policy's funds with the court. By doing so, the court alleviated the carrier of the risk of finding themselves amidst competing claims between the insured’s bankruptcy trustee and the directors and officers of the insured.

Read More >>

A PROVISION FOR TREATMENT OF RELATED CLAIMS SAVES A RELATED CLAIM EXCLUSION FROM DENYING COVERAGE

Seritage Growth Properties v. Endurance American Ins. Co., No. N21C-03-015 MMJ CCLD (Del. Super. Ct 2023)

In the underlying litigation, a department store created a Real Estate Investment Trust (“REIT”) as its subsidiary and insured it under a Directors and Officers (“D&O”) liability policy. Immediately after its creation, the REIT appointed as its president someone who held a leadership role within the department store.

Read More >>

APPRAISAL ACTION IS NOT A SECURITIES CLAIM UNDER DELAWARE LAW

Stillwater Mining Co. v. Nat’l Union Fire Ins. Co. of Pittsburg, PA, No. N20C-04-190 (Del. 2023)

A group of stockholders filed an appraisal action seeking a post-merger appraisal of shares. The Insured sought coverage under its Directors and Officers Liability (“D&O”) policy, but the carrier denied coverage.

Read More >>

ILLINOIS COURTS CONTINUE TO FIND POTENTIAL BIPA COVERAGE UNDER GENERAL LIABILITY POLICIES

Thermoflex Waukegan, LLC v. Mitsui Sumitomo Ins. USA, Inc., 2023 U.S. Dist. LEXIS 9282 (January 23, 2023)

An Illinois federal court ruled in favor of an insured automotive accessory company in a suit against its umbrella insurer, finding that although a duty to defend against violations of the Biometric Information Privacy Act (“BIPA”) existed, that duty had not yet been triggered.

Read More >>

CYBER CORNER

Click to read the following cases:

- WIRELESS CARRIER FACES TWO CONSUMER CLASS ACTIONS FOLLOWING SECOND DATA BREACH

- MAJOR RANSOMWARE GANG DISRUPTED BY FBI, FOREIGN LAW ENFORCEMENT

Read More >>

EMPLOYMENT CORNER

Click to read the following cases:

- PAY BIAS SUIT DISMISSED AGAINST RESEARCH-BASED BIOPHARMACEUTICAL COMPANY

- COURTS BEGIN TO QUESTION IF SUMMARY JUDGMENT HAS BEEN MISUSED UNDER RULE 56 OF ERISA

Read More >>

SEC CORNER

Click to read the following cases:

- SEC PROPOSES RULE TO PROTECT AGAINST CONFLICTS OF INTEREST

- JANUARY 2023 NOTEWORTHY ENFORCEMENT ACTIONS FILED

- JANUARY 2023 NOTEWORTHY SETTLEMENTS AND JUDGEMENTS

Read More >>

SHAREHOLDER CORNER

Click to read the following cases:

- JANUARY 2023 SECURITIES CLASS ACTION FILINGS

Read More >>

DELAWARE COURT OF CHANCERY RULES THAT OFFICERS HAVE DUTY OF OVERSIGHT WITH RESPECT TO SEXUAL MISCONDUCT CASE, CALIFORNIA COURT ADDRESSES SIMILAR ISSUE

In re McDonald’s Corporation Stockholder Derivative Litigation, No. 2021-0324-JTL (Del. Jud. Jan. 25, 2023)

Luke Kahnert, et al. v. Robert A. Kotick, et al., No. CV 21-8968PA (U.S. C.D. Cal. Jan. 17, 2023)

In Delaware, the Court of Chancery held, for the first time, that corporate officers may have the same duties of care and oversight as corporate directors. The matter arises from a derivative lawsuit brought by shareholders against the company’s board, the former CEO and the former Global Chief People Officer alleging breaches of fiduciary duty for failing to prevent a culture of sexual harassment and misconduct.

Allegations included a Caremark claim for breach of the duty of oversight. The former officers sought to defeat the duty of oversight by arguing that Delaware law has not previously recognized such Caremark claims against corporate officers.

In its opinion, the Vice-Chancellor noted that in Caremark, the Delaware Supreme Court held that the duties of officers are the same as the duties of directors. Thus, officers may also owe a duty of oversight. Under Delaware law it is presumed that directors and officers act in good faith, thus a complaint must allege facts sufficient to support an inference of bad faith intent. The subject derivative complaint alleged that the former officer was personally engaged in acts of sexual harassment, which led to discipline, and later termination, and thus equated to a breach of the duty of oversight.

The court relied on the “Reg Flags Rule” which states that directors OR officers could be liable for failing to take action if they were aware of red flags indicating wrongdoing and consciously chose not to act. The Red-Flag Obligation simply recognizes that the officers who are running the business on a full-time basis have a duty to address or report upward. The complaint described that the former officer breached the duty of oversight, by alleging that the former officer knew about evidence of sexual misconduct and acted in bad faith by consciously disregarding the duty to address the misconduct. The court stated that it is reasonable to infer that an officer consciously ignored red flags about similar behavior by others when they themselves engaged in such acts. Thus, these particular officers, like directors, can be held liable for a breach of the duty of oversight.

In another recent decision, a district court in California addressed the duty of oversight in connection with similar allegations. Much like the Delaware case above, the complaint alleged that the company created a hostile work environment which resulted in employees suffering from sexual harassment, physical assault, and sex discrimination. Unlike the company in Delaware, the company involved in the California case had a working oversight plan in place that was capable of receiving complaints and properly addressing and resolving matters. Thus, the court reasoned that while the company had a duty of oversight, the duty was not breached in that particular circumstance because the company had an adequate system in place designed to safeguard and watchdog such events.

The Takeaway

Prior to this decision, no Delaware court had held that an officer could be sued for an alleged Caremark violation. It remains to be seen if this decision will be appealed to the Delaware Supreme Court for further adjudication. For now, officers may be held accountable for such claims which, in all likelihood, would involve potential erosion of Side A limits for defense or settlement of such Claims.

BUMP-UP EXCLUSION PRECLUDES COVERAGE FOR MERGER LITIGATION SETTLEMENT

Komatsu Mining Corp. v. Columbia Casualty Co., 2023 U.S. App. Lexis 1639, No. 2:18-CV-02034 (7th Cir. 2023)

A federal appeals court held that an “inadequate consideration” or “Bump-Up” exclusion in a primary Directors & Officers Liability (“D&O”) policy precluded coverage for a settlement arising from a merger.

Litigation ensued following the completion of a merger between two manufacturers of heavy mining equipment. The shareholders of one of the companies alleged violations of Section 14 of the Securities Exchange Act over the failure of the company to disclose internal projections of future growth. Specifically, the shareholders alleged that these omissions rendered the proxy statements fraudulent and misleading. As a result, the shareholders argued that the directors breached their duties by failing to maximize the price that the shareholders stood to receive. The litigation ultimately settled, and the company sought coverage for the settlement under its D&O policy.

The insurers denied coverage under an “inadequate consideration” exclusion in the primary D&O policy. The exclusion provided that there was no coverage for any “amount of any judgment or settlement of any Inadequate Consideration Claim other than Defense Costs.” Furthermore, the exclusion did not cover “that part of any Claim alleging that the price or consideration paid or proposed to be paid for the acquisition or completion of the acquisition of all or substantially all the ownership interest in or assets of an entity was inadequate.”

The company sued its insurers, arguing that the underlying claim could not have been about “inadequate consideration” because that type of action is governed by state, not federal, law. However, the court reasoned that a Section 14 action alleges false or inadequate disclosure, and the reason the disclosure was inadequate was that the company failed to reveal that the price was too low. Accordingly, the court determined that the proxy statements induced shareholders to vote in favor of a merger at a less advantageous price, which constituted an “inadequate consideration claim” under the policy’s definition. The court reasoned that the loss from any legal wrong, whether state or federal, depended on a conclusion that the price offered in the merger was too low; thus, the allegations fit squarely within the inadequate consideration exclusion in the policy.

The Takeaway

Whether a claim involving a settlement arising out of an M&A transaction will be covered requires a careful assessment of, among other things, the exclusionary language at issue, the particular type of transaction at issue, and the nature of the claim against the policyholder. Furthermore, careful analysis of the wording of a bump-up exclusion in an insurance policy is crucial. A knowledgeable insurance broker and claims attorney are critical to navigating these complex issues.

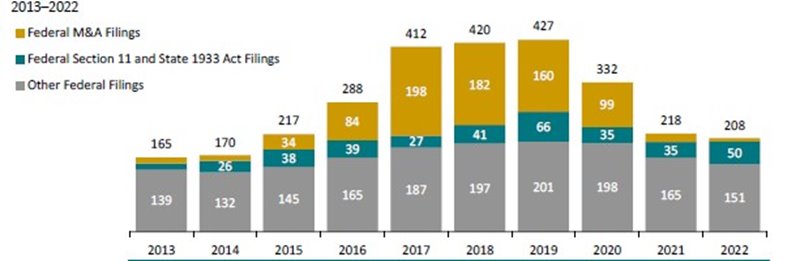

2022 TRENDS IN SECURITIES CLASS ACTION LITIGATION

Trends in securities class action litigation in 2022 showed drastic differences from years prior. For the fourth consecutive year, federal filings have declined because of fewer merger-objection and Rule 10b-5 cases being filed—from 431 cases filed in 2018 to only 205 filed in 2022. We also saw fewer cases resolved in 2022 than in 2021, a decline driven by the decrease in dismissed non-merger-objection and non-crypto unregistered securities cases.

While 2022 was a record-setting year for the number of settled cases, there was an even larger decline in dismissed non-merger-objection and non-crypto unregistered cases, which led to a decline in overall resolutions. As of December 31, 2022, a larger portion of the cases filed since 2015 have been dismissed rather than settled. This remains consistent with historical trends which have shown that settlements occur later in the litigation cycle, while dismissals tend to occur in the earlier stages. In comparison to 2021, the number of aggregate settlements for 2022 increased by over 50%, increasing the average settlement value by over 70%.

Source: Cornerstone

DELAWARE INCREASES SCRUTINY OF SPAC DISCLOSURES

Delman v. GigAcquisitions3, LLC, No. 2021-0679-LWW, 2023 Del. Ch. LEXIS 1 (Del. Ch. Jan. 4, 2023).

Delaware toughened its stance on Special Purpose Acquisition Companies (“SPACs”) and subjected them to more scrutiny. Shareholders of a SPAC which acquired an electric vehicle start-up, claimed that it fared poorly for investors despite optimistic financial projections issued before the merger. The complaint alleged that investors were denied material information needed to decide whether they should have redeemed their shares before the SPAC merger. The court concluded that the reduced share value stemmed from various costs, including fund equity compensation for directors and other measures taken by the SPAC to close the deal.

In denying the SPAC’s motion to dismiss the court found that the SPAC pre-merger disclosures were lacking sufficient information. Specifically, the proxy did not accurately disclose information regarding the net cash per share or, in other words, how the merger transaction diluted the value of investor’s share.

By subjecting SPAC mergers to a Delaware fairness standard, the court has placed the burden on the company to demonstrate the fairness of the transaction. Opponents of the ruling saw this decision as opening SPACs up to more litigation as well as discouraging mergers from getting the necessary approval from shareholders.

A JOINT VENTURE MEMBER SHOULD BE ABLE TO PRESENT ANY INFORMATION TO THE APPRAISER

A Delaware court ruled in favor of the majority owner of a joint venture company, in a dispute that alleged that the majority owner inappropriately intervened with the appraisal process of the minority company.

The complaint alleged that the majority owner exploited the minority-owned company for their own benefit, exercising bad faith that resulted in the decrease of the minority owned company's fair market value. The minority owners requested the court to provide a relief from the valuation process, synergy information, and the decrease in the joint venture's value that followed the majority owner's abuse of control over the joint venture.

Specifically, the minority owners argued that the majority owner deprived them of access to the information that would have enabled the appraiser to determine the joint venture’s fair market value, such as long-range plans, synergies and decreases in the joint venture’s value. In response, the majority owner argued that the information the minority owner was seeking was outdated and irrelevant.

The court ruled that each side was entitled to present any information they considered relevant to the appraiser, leaving the determinations of outdatedness and relevance for the appraiser to make.

CONSTRUCTIVE NOTICE NOT SUFFICIENT IN THE CLAIMS MADE AND REPORTED WORLD

Evanston Ins. Co. v. Rodriguez Eng'g Labs., No. 1:21-CV-01129-RP, 2023 U.S. Dist. LEXIS 9885 (W.D. Tex. Jan. 20, 2023)

A Texas federal court ruled that an engineering firm (the “Company”) lost its coverage when it failed to timely notify its excess professional liability (“PL”) carrier of a claim timely. In the underlying suit, the company was accused of defective work on a project. The Company did not provide a direct notice to its excess insurance carrier, and the latter denied coverage.

At issue was a “claims made and reported” policy that provided that it was “limited to those claims that [were] first made against the Insured and reported to Underwriters during the Policy Period.” The Company provided a timely notice to its broker. The broker notified the primary, but not the excess carrier because the broker was waiting for the primary carrier’s determination of the claim’s size and scope. By the time the excess carrier was notified, the policy had expired. Accordingly, the excess carrier denied coverage due to untimely notice. In response, the Company argued that, in light of agency law and the prior course of dealings between the parties, the notice to the broker should have been deemed as sufficient, or constructive notice to the carrier. In providing the notice to the broker, and not the carrier, the Company relied on the producer agreement which stated that the “[broker] will (i) immediately notify [the carrier] of all claims, suits, and notices.”

The court rejected the Company’s constructive notice theory. It pointed to the producer agreement, highlighting that the language of the agreement did not support the notion that the broker acted as the carrier’s alter-ego, or agent, for purposes of the receipt of the company’s claims. According to the court, the agreement did not provide the broker with the actual authority to receive claims on behalf of the carrier. Specifically, although the agreement stated that the broker will immediately forward all claims or proceedings, this promise was “not an express grant of authority to [broker] to receive claims on [insurer’s] behalf.” Therefore, the Company was denied coverage due to failure to notify its excess carrier directly of the defective work claim.

The Takeaway

The consequences of untimely notice under “claims-made-and-reported” policies often seem inequitable. Such results are often amplified when insureds pay high premiums. Accordingly, best practices dictate that clients alert the carriers and brokers early and often of Claims and potential claims.

FAILURE TO COMPLY WITH NOTICE REQUIREMENT COSTS BANK EXCESS COVERAGE

Heritage Bank of Commerce v. Zurich Am. Ins. Co., No. 21-cv-10086-RS, 2023 U.S. Dist. LEXIS 383 (N.D. Cal. Jan. 3, 2023)

A California district court ruled against a bank in its effort to compel coverage from two layers of excess insurance. The insured bank failed to provide proper notice to the excess carriers in the tower of insurance during the policy period.

The bank tendered the matter to its primary carrier but failed to provide notice to the excess carriers during the policy period. As part of its renewal process, it advised the excess carriers’ underwriters of a legal hold letter that it characterized as a “nuisance incident.” No notice was provided to the claims department for the excess tower until several months after the policy period expired, and only when the insured began receiving lawsuits related to the incident. The excess carriers denied the matter, citing failure to comply with the notice requirements, and coverage litigation ensued.

The insured attempted to argue that its notice to the underwriting department constituted proper notice, but the court was not persuaded. The policy unambiguously required notice to the claims department during the policy period. However, the insured failed to comply. The court explained that ignoring the notice requirement in the insurance policy would seriously undermine insurers’ ability to ever set its own procedures.

The bank argued that the court should consider the substantial compliance doctrine. The doctrine would allow “equitable excuse of a condition precedent” because the bank advised the insurer of the matter, although it did so without full compliance with the policy’s notice provisions. The court rejected this argument, too, finding that the policy’s requirement of who the notice must be directed to was a bright line requirement that must be complied with. Ultimately, the court dismissed the Bank’s coverage suit against the excess insurers.

The Takeaway

This case is yet another example of the critical importance of providing proper notices of claims including to excess carriers of any time a claim is tendered to the primary carrier. Had notice been made to the excess carriers in a timely fashion and as required by the policy terms, coverage likely would not have been at issue. In claims-made and reported policies at the time when the claim is received, a timely (and sufficient) notice of claims to both the primary and excess carriers is necessary even if the claim is not expected to ever impact the excess layers. Failure to do so can be a costly mistake when and if the excess coverage is implicated.

CONTRADICTORY COMPLAINTS LEADS TO DISMISSAL ON ALL ALLEGATIONS

Underwood v. Coinbase Glob., Inc., 2023 U.S. Dist. LEXIS 17201 (S.D.N.Y. Feb. 1, 2023)

A New York federal court ruled in favor of a crypto exchange (“Exchange”) after cryptocurrency buyers (“Buyers”) failed to prove that the exchange was an “immediate seller” of securities. This action was brought on behalf of a nationwide class consisting of all persons or entities who transacted in securities on the Exchange’s trading platform.

In the original complaint, the Buyers included the Exchange’s User Agreement (“Agreement”) which permitted the court to consider the Agreement in conjunction with the allegations. Eventually, the Buyer’s revised their alleged violations under the Securities Act and the Exchange Act, including Control-Person Liability.

To recover under the Securities Act the buyer had to show that the Exchange (1) was the direct seller of the securities; or (2) had actively solicited the sale of the securities for financial gain. The Buyers argued that the Exchange was the direct seller because all assets were deposited into a centralized wallet, and thus had title to all assets. In response, the court looked to the language of the Agreement which provided that all digital assets shall at all times remain with the Buyer in their currency wallet and shall not transfer to the Exchange. The court held that the Buyer’s amended allegations contradicted what was originally alleged, and that the Buyers could not plead around the Agreement. The Buyers also argued the Exchange actively participated in the sale of securities because it provided various services. The services included descriptions of securities and promotions to increase trading volume. The court held that these activities were merely marketing efforts and were therefore insufficient to establish active solicitation.

Control-Person Liability under the Securities Act provides liability against those who control, directly or indirectly, an entity or individual that violates the Securities Act. Because the Exchange never directly or indirectly controlled the securities at issue, the court held there was no violation under the Securities Act, thus no Control-Person Liability violation.

The Buyer’s revised allegations also claimed that the Exchange had violated the Securities and Exchange Act of 1934 by involving a contract that concerned a prohibited transaction. The court stated that the Agreement was not unlawful because it did not necessitate illegal acts. To strengthen the point, the court added that the Buyers continued to use the Exchange even after filing the original complaint. The court relied on the Agreement which was incorporated into the Buyer’s original allegations.

The Takeaway

Given the decentralized nature of cryptocurrency, the debate surrounding whether cryptocurrency is a security is still unsettled. Above is another example of a court holding that cryptocurrency is not a security because a single entity or individual does not have sufficient control over the securities being exchanged.

IN A COMPETING CLAIMS SCENARIO, INTERPLEADER IS APPROPRIATE

QBE Specialty Ins. Co. v. Kane, No. 22-00450 SOM-KJM, 2023 U.S. Dist. LEXIS 14705 (D. Haw. Jan. 27, 2023)

A Hawaiian court agreed to deposit the remainder of a directors and officers policy's funds with the court. By doing so, the court alleviated the carrier of the risk of finding themselves amidst competing claims between the insured’s bankruptcy trustee and the directors and officers of the insured.

At issue was a directors and officers (“D&O”) liability policy which provided that advancements must be made “on a current basis.” However, the policy’s language did not resolve any substantive right to coverage or how to address conflicting claims. After the insured filed for bankruptcy, the bankruptcy trustee filed various claims against the directors and officers of the insured. As a result, a number of parties sought carriers’ funds to cover their defense costs and they were deemed to have coverage for such claims under the terms of the policy. Thus, it became apparent that the carrier faced competing claims against limited policy funds. To shield itself from future litigation, the carrier filed an interpleader action, or, in other words, asked the court to allow it to deposit the policy limits and for a release from involvement in a battle among claimants at which the carrier had no stake.

The insured parties who were competing for the funds disagreed with the carrier, arguing that the carrier filed the action in bad faith. The insureds also argued that the Policy’s advancement provision required the funds to be paid to the first claimant who sought them.

The court agreed to deposit the funds with the court, thereby relieving the carrier of future risks that competing claims may entail. The court rejected the insureds arguments that the advancement or the priority of payments provision of the policy provided sufficient guidance to resolve carrier’s concerns. The court explained that the carrier had a low bar to meet, as they only needed to show that its fear of multiple liability was more than conjectural, even when adverse claims are not particularly strong. According to the court, the carrier acted in good faith as they faced a real threat of multiple competing claims in the light of adverse claims and the reality of adverse claimants.

The Takeaway

Competing demands that are likely to exhaust the policy limits are unfortunate for all parties. It is hard to account for the resolution of such matters in the language of insurance policies as they often cause various policy provisions to clash. In those situations, interpleader actions can help the carriers to perform their obligations without risking exposure to future litigation.

A PROVISION FOR TREATMENT OF RELATED CLAIMS SAVES A RELATED CLAIM EXCLUSION FROM DENYING COVERAGE

Seritage Growth Properties v. Endurance American Ins. Co., No. N21C-03-015 MMJ CCLD (Del. Super. Ct 2023)

In the underlying litigation, a department store created a Real Estate Investment Trust (“REIT”) as its subsidiary and insured it under a Directors and Officers (“D&O”) liability policy. Immediately after its creation, the REIT appointed as its president someone who held a leadership role within the department store.

To raise funds, the president authorized a Rights Offering. The Offering funded the REIT’s purchase of almost three hundred properties from the department store. After purchasing these properties, the REIT proceeded to lease them back to the department store (the “leaseback transaction”). Prior to the transaction, the REIT had D&O insurance.

Following the transaction, the department store filed and later settled a derivative suit against various directors and officers alleging breach of fiduciary duties (the “Derivative Action”). Several years later, the department store filed for bankruptcy. That proceeding led to the department store’s unsecured creditors filing an adversary proceeding against REIT and its directors and officers involved in the transaction (the “Adversary Proceeding”). The creditors alleged that the REIT’s leaseback transaction was unfair as it was a direct result of artificially low appraisals of real estate.

Initially, the primary insurer, granted coverage for the Adversary Proceeding. However, the department store’s insurance broker contacted the insurer and requested a reevaluation of the claim. Following the claim’s reevaluation, the insurer denied coverage because it determined the Adversary Proceeding and the Derivative Action were related claims and thus barred coverage under this policy. Coverage litigation ensued.

The carrier argued that two actions were related and held that the Adversary Proceeding would be outside the policy period; effectively nullifying coverage. The insured, however, argued that the two claims were not related because they were brought by two different parties. The court held that both the Adversary Proceeding, and the Derivative Action arose out of and relied on the initial sale-and-leaseback transaction. The court went further and pointed to the language in the policy which stated that “all Related Claims shall be deemed a single Claim first made during the Policy Period in which the earliest of such Related Claims was either first made or deemed to have been first made in accordance” with the policy’s reporting requirements. The court held that the policy would provide coverage for future claims that are related to claims deemed first filed under the policy. Therefore, even though the Adversary Proceeding and the Derivative Action were related, the policy language permits treating the Adversary Proceeding as a claim first made within the policy period.

APPRAISAL ACTION IS NOT A SECURITIES CLAIM UNDER DELAWARE LAW

Stillwater Mining Co. v. Nat’l Union Fire Ins. Co. of Pittsburg, PA, No. N20C-04-190 (Del. 2023)

A group of stockholders filed an appraisal action seeking a post-merger appraisal of shares. The Insured sought coverage under its Directors and Officers Liability (“D&O”) policy, but the carrier denied coverage. The carrier took the position that although shareholders have a statutory right in the state of Delaware to seek an appraisal of their shares, they were not required to also allege violations of securities laws in order to exercise their rights. The carrier asserted that the appraisal proceedings did not meet the Policy’s definition of Securities Claim.

The Insured argued that Delaware law applied and likely did so in an attempt to benefit from the Chancery Court’s inclination to favor policyholders (and to find in favor of coverage). Accordingly, the Insureds asked the court to apply Delaware law. However, during the pendency of the coverage litigation, the Delaware Supreme Court issued a ruling in another case which held that appraisal actions were not a Securities Claim under a D&O insurance policy. Therefore, the appraisal action likely would not meet the definition of Securities Claim in most D&O policies. In response to the new decision, the Insured argued that Montana law, rather than Delaware law was applicable. The Insured argued that Delaware law should not apply because the complaint dealt with the issue of claims handling, rather than policy coverage. The court disagreed and after a choice of law analysis held that (1) the dispute was mainly a contract dispute as it involved the interpretation of obligations and rights under the policy, and (2) the insured failed to show that Montana had a relatively greater interest than Delaware.

The court noted that the state of incorporation was the center of gravity in a D&O policy. Furthermore, the court cited to a Montana endorsement in the policy which stated a “mediator or arbitrators shall consider the general principles of law of the state where the insured is incorporated.” The Insured argued that its presence in Montana was sufficient to tip the balance and thus Montana law was applicable. However, the court disagreed and found that the emphasis on physical location underrated the significance of the company’s status as a Delaware corporation, thus there was no coverage under the insured’s D&O policy.

ILLINOIS COURTS CONTINUE TO FIND POTENTIAL BIPA COVERAGE UNDER GENERAL LIABILITY POLICIES

Thermoflex Waukegan, LLC v. Mitsui Sumitomo Ins. USA, Inc., 2023 U.S. Dist. LEXIS 9282 (January 23, 2023)

An Illinois federal court ruled in favor of an insured automotive accessory company in a suit against its umbrella insurer, finding that although a duty to defend against violations of the Biometric Information Privacy Act (“BIPA”) existed, that duty had not yet been triggered. The insured tendered the claim to its general liability (“GL”) carriers, including both an umbrella and excess policy.

The primary GL carrier was required to provide a defense to the insured under that policy. Coverage under the excess and umbrella policies were raised separately by the parties for the court to review. Notably, the excess and umbrella policies required the carrier to defend the insured for damages that may be covered under certain “personal and advertising injury” coverage grants. At issue was whether exclusions for “Data Breach Liability,” “Statutory Violations,” and “Employment Related Practices” applied to bar both coverage and the duty to defend.

The court first reviewed the Statutory Violation Exclusion, which specifically excluded claims arising out of violations of the Telephone Consumer Protection Act, Can-Spam Act and Fair Credit Reporting Act, as well as “other related” state and federal laws. As BIPA was dissimilar to the specific statutes referenced in the exclusion, the court found it ambiguous and inapplicable. As to the Data Breach Exclusion, the court also found it ambiguous and inapplicable as a breach of data was not at issue. Finally, the court held that this matter did not fall within the Employment Related Practices Exclusion. The court relied on prior decisions which previously held that BIPA does not fall within the purview of the exclusion, as it is a workplace policy that applies to everyone the same way and is not directed at a specific employee.

Based on the above, the court found that the insured owed a duty to defend, which would be triggered upon exhaustion of the primary GL policy limits.

The Takeaway

While this matter involved general liability coverage, the trend seems to be that courts are requiring GL carriers to provide a defense for BIPA matters despite various commonly raised exclusions. While insurance carriers continue to try and limit exposure for BIPA matters under Management Liability policies, it is critical to tender and pursue defense obligations for these matters to the GL and any other potentially applicable policies.

Cyber Corner

WIRELESS CARRIER FACES TWO CONSUMER CLASS ACTIONS FOLLOWING SECOND DATA BREACH

Baughman v. T-Mobile US Inc., Case No. 2:23-cv-00477, (C.D. Cal.) and Cortazal v. T-Mobile US Inc., 3:23-cv-01220, (N.D. Fla.)

Consumers in two states have filed proposed class action lawsuits against a wireless telecommunications carrier alleging harm following a second data breach at the company, which potentially impacted approximately 37 million subscribers.

MAJOR RANSOMWARE GANG DISRUPTED BY FBI, FOREIGN LAW ENFORCEMENT

The Federal Bureau of Investigation (FBI), in cooperation with its German and Dutch counterparts, seized servers and websites belonging to Hive, a prominent ransomware crime syndicate, terminating hundreds of extortion threats and saving its victims about $130 million in potential ransom payments, according to a statement released by the U.S. Department of Justice (DOJ).

PAY BIAS SUIT DISMISSED AGAINST RESEARCH-BASED BIOPHARMACEUTICAL COMPANY

Jirek v. Astrazeneca Pharm. LP, No. 21 C 6929, 2023 U.S. Dist. LEXIS 12667 (N.D. Ill. Jan. 25, 2023)

An Illinois court ruled in favor of a Biopharmaceutical Company (the “Company”) in a suit where three sales employees sued the Company for discriminating against them based on their sex. Specifically, the employees argued that, in violation of various federal and state laws, male employees of the Company received higher compensation than their female counterparts.

COURTS BEGIN TO QUESTION IF SUMMARY JUDGMENT HAS BEEN MISUSED UNDER RULE 56 OF ERISA

Tekmen v. Reliance Standard Life Ins. Co., 55 F.4th 951 (4th Cir. 2022)

Under the Employee Retirement Income Security Act (ERISA), the process of summary judgment—judgment entered by court without a full trial, based on the ERISA benefit file and the law—has been a long-standing topic of discussion. The issue recently came into play in a case that involved a claim for long-term disability benefits.

SEC Corner

SEC PROPOSES RULE TO PROTECT AGAINST CONFLICTS OF INTEREST

In response to past market abuse, such as the 2008 financial crisis, the SEC has made an ongoing effort to protect investment transactions. The SEC is revisiting an earlier proposal that was never finalized, to implement a provision under the Dodd Frank Act prohibiting underwriters, agents, purchasers, sponsors, subsidiaries, and affiliates of asset-backed securities from engaging in transactions that would result in material conflicts of interest.

JANUARY 2023 NOTEWORTHY ENFORCEMENT ACTIONS FILED

|

Director/Officer |

Role |

Company |

|

Cooper J. Morgenthau |

CFO |

African Gold Acquisition Corp. |

|

Samuel Bankman-Fried |

CEO, Co-founder |

FTX Trading Ltd. |

|

Zixiao (Gary) Wang |

CTO, Co-founder |

FTX Trading Ltd. |

|

Caroline Ellison |

CEO |

Alameda Research |

|

Director/Officer |

Role |

Company |

|

Cooper J. Morgenthau |

CFO |

African Gold Acquisition Corp. |

|

Samuel Bankman-Fried |

CEO, Co-founder |

FTX Trading Ltd. |

|

Zixiao (Gary) Wang |

CTO, Co-founder |

FTX Trading Ltd. |

|

Caroline Ellison |

CEO |

Alameda Research |

JANUARY 2023 NOTEWORTHY SETTLEMENTS AND JUDGMENTS

|

Amount |

Director/Officer |

Role |

Company |

|

$ 69,000.00 |

Kurt W. Streams |

CFO |

SITO Mobile, Ltd. |

|

$ 50,000.00 |

Gerard R. Hug |

CEO |

SITO Mobile, Ltd. |

|

Amount |

Director/Officer |

Role |

Company |

|

$ 69,000.00 |

Kurt W. Streams |

CFO |

SITO Mobile, Ltd. |

|

$ 50,000.00 |

Gerard R. Hug |

CEO |

SITO Mobile, Ltd. |

Source: U.S. Securities and Exchange Commission

Financial

Source: Stanford Law School Securities Class Action Clearinghouse

ABOUT ALLIANT INSURANCE SERVICES

Alliant Insurance Services is the nation’s leading specialty broker. In the face of increasing complexity, our approach is simple: hire the best people and invest extensively in the industries and clients we serve. We operate through national platforms to all specialties. We draw upon our resources from across the country, regardless of where the resource is located.

Contributors

Abbe Darr, Esq.

Claims Attorney

abbe.darr@alliant.com

David Finz, Esq.

Claims Attorney

david.finz@alliant.com

Isabel Arustamyan

Claims Advocate

isabel.arustamyan@alliant.com

Jacqueline Vinar, Esq.

Claims Attorney

jacqueline.vinar@alliant.com

Jaimi Berliner, Esq.

Claims Attorney

jaimi.berliner@alliant.com

Katherine Puthota

Senior Claims Advocate

katherine.puthota@alliant.com

Malia Shappell, Esq.

Claims Attorney

malia.shappell@alliant.com

Matia Marks, Esq.

Claims Attorney

matia.marks@alliant.com

Michael Radak, Esq.

Claims Attorney

michael.radak@alliant.com

Robert Aratingi

Senior Claims Advocate

robert.aratingi@alliant.com

Robert Hershkowitz, Esq.

Claims Attorney

robert.hershkowitz@alliant.com

Steve Levine, Esq.

Claims Attorney

slevine@alliant.com